Recent News

02/20/2026

To maximize — or not to maximize — depreciation deductions on your 2025 tax return

The deadlines for filing 2025 tax returns (or extensions) are fast approaching. Although most tax planning moves must be completed by December 31 of the tax year, there are some decisions you can make when filing your return that can save taxes now or in the future. One such decision is whether to claim accelerated depreciation breaks. Depreciation Basics For assets with a useful life of more than one year, the cost generally must be depreciated over a period of years (unless accelerated depreciation breaks are available). In other words, taxpayers can deduct only a portion of the asset’s cost...

Stay up to date! Subscribe to our future blog posts!

10/06/2023

What types of expenses can’t be written off by your business?

If you read the Internal Revenue Code (and you probably don’t want to!), you may be surprised to find that most business deductions aren’t specifically listed. For example, the tax law doesn’t explicitly state that you can deduct office supplies and certain other expenses. Some expenses are detailed in the tax code, but the general rule is contained in the first sentence of Section 162, which states you can write off “all the ordinary and necessary expenses paid or incurred during the taxable year in carrying on any trade or business.” Basic definitions In general, an expense is ordinary if...

09/29/2023

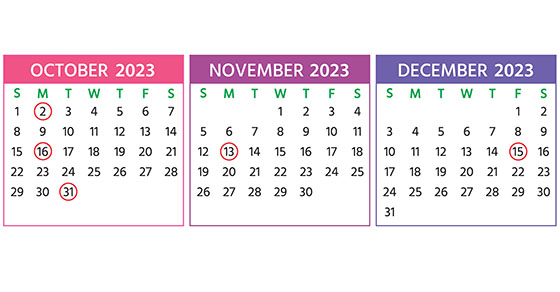

2023 Q4 tax calendar: Key deadlines for businesses and other employers

Here are some of the key tax-related deadlines affecting businesses and other employers during the fourth quarter of 2023. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. Contact us to ensure you’re meeting all applicable deadlines and to learn more about the filing requirements. Note: Certain tax-filing and tax-payment deadlines may be postponed for taxpayers who reside in or have businesses in federally declared disaster areas. Monday, October 2 The last day you can initially set up a SIMPLE IRA plan, provided you (or any predecessor employer) didn’t previously maintain...

09/22/2023

It’s important to understand how taxes factor into M&A transactions

In recent years, merger and acquisition activity has been strong in many industries. If your business is considering merging with or acquiring another business, it’s important to understand how the transaction will be taxed under current law. Stocks vs. assets From a tax standpoint, a transaction can basically be structured in two ways: 1. Stock (or ownership interest) sale. A buyer can directly purchase a seller’s ownership interest if the target business is operated as a C or S corporation, a partnership, or a limited liability company (LLC) that’s treated as a partnership for tax purposes. The now-permanent 21% corporate federal...

09/15/2023

Spouse-run businesses face special tax issues

Do you and your spouse together operate a profitable unincorporated small business? If so, you face some challenging tax issues. The partnership issue An unincorporated business with your spouse is classified as a partnership for federal income tax purposes, unless you can avoid that treatment. Otherwise, you must file an annual partnership return, on Form 1065. In addition, you and your spouse must be issued separate Schedule K-1s, which allocate the partnership’s taxable income, deductions and credits between the two of you. This is only the beginning of the unwelcome tax compliance tasks. The self-employment (SE) tax problem The SE...

09/08/2023

Could your business benefit from interim financial reporting?

When many business owners see the term “financial reporting,” they immediately think of their year-end financial statements. And, indeed, properly prepared financial statements generated at least once a year are critical. But engaging in other types of financial reporting more frequently may help your company stay better attuned to the nuances of running a business in today’s inflationary and competitive environment. Spot trends and trouble Just how often your company should engage in what’s often referred to as “interim” financial reporting depends on factors such as its size, industry and operational complexity. Nevertheless, monthly, quarterly and midyear financial reports can enable...

09/01/2023

Guaranteeing a loan to your corporation? There may be tax implications

Let’s say you decide to, or are asked to, guarantee a loan to your corporation. Before agreeing to act as a guarantor, endorser or indemnitor of a debt obligation of your closely held corporation, be aware of the possible tax implications. If your corporation defaults on the loan and you’re required to pay principal or interest under the guarantee agreement, you don’t want to be caught unaware. A business bad debt If you’re compelled to make good on the obligation, the payment of principal or interest in discharge of the obligation generally results in a bad debt deduction. This may...